In a world where cash can be a pressing need at the drop of a hat, the ability to secure a personal loan in under 24 hours is no longer a luxury—it’s becoming a mainstream expectation. Across the United States, consumers are turning to fintech platforms that promise instant approvals, minimal paperwork, and funding delivered directly into their bank accounts within a single business day.

While the concept of quick loans isn’t new, the pace at which technology has advanced in 2026 has turned what used to be a weeks‑long process into an almost instantaneous transaction. This shift is driven by a confluence of AI‑powered underwriting, real‑time data feeds, and a growing appetite among borrowers for speed and convenience.

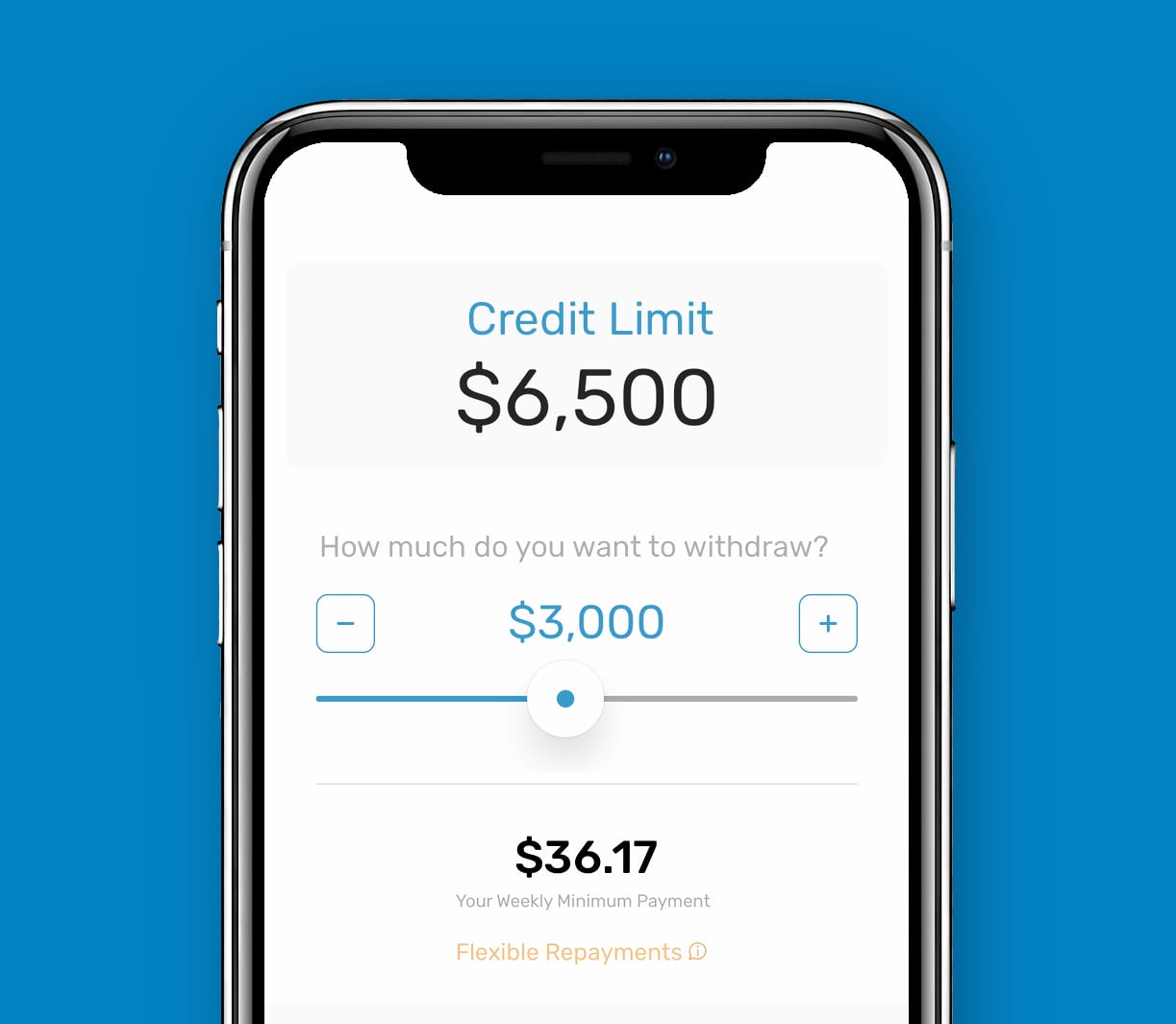

One platform that exemplifies this trend is Jetzloan, which has been quietly gaining traction among consumers seeking rapid funding without the high fees often associated with payday lenders. By integrating machine learning algorithms that analyze a borrower’s financial behavior, Jetzloan can provide approval decisions in minutes, delivering funds to the borrower’s account by the next business day.

Why Speed Matters: The Consumer Perspective

When unexpected expenses arise—whether it’s an emergency medical bill, a sudden car repair, or a last‑minute trip—waiting weeks for a loan can feel like a death sentence. Many borrowers report that the anxiety of delayed funding outweighs concerns about higher interest rates.

- Immediate Relief: Quick loans provide instant financial breathing room.

- Convenience: Applications are completed online, often in less than 10 minutes.

- Flexibility: Borrowers can choose repayment terms that fit their cash flow.

According to a recent Built In analysis, fintech lenders have seen a 35% rise in users seeking loans with funding times under one business day. This surge underscores the market’s appetite for speed and simplicity.

The Technology Behind Instant Loans

At the heart of these rapid approvals lies artificial intelligence. By ingesting data from credit bureaus, bank statements, employment records, and even social media activity, AI models can assess risk with unprecedented precision. This allows lenders to offer competitive rates to borrowers who might otherwise be deemed high‑risk by traditional banks.

For example, Avant uses a proprietary algorithm that evaluates more than 300 data points. The result is an approval decision in under two minutes and funding within one business day for many applicants.

Regulatory Landscape: Balancing Speed with Safeguards

The rapid growth of fintech lenders has prompted regulators to revisit consumer protection rules. In 2026, the Consumer Financial Protection Bureau (CFPB) released guidelines that require clear disclosure of interest rates, fees, and repayment terms for all instant‑funding products.

- Transparency: Lenders must present APRs in plain language.

- No Hidden Fees: Any additional charges must be disclosed upfront.

- Grace Periods: Borrowers should receive a minimum 30‑day grace period before interest accrues.

These measures aim to protect consumers from predatory practices while preserving the convenience of digital lending. Built In notes that compliance has become a differentiator among fintech companies, with those who invest in robust disclosure systems gaining consumer trust.

Comparing the Big Players: A Quick Look at Market Leaders

| Lender | Funding Time | Typical APR | Minimum Credit Score | Key Feature |

|---|---|---|---|---|

| Avant | 1–2 days | 13.99% – 25% | 580 | AI‑driven underwriting |

| Affirm | Instant (point of sale) | 8% – 30% | 650 | Installment plans at retailers |

| Empower | 1–2 days | 15% – 24% | 600 | No‑interest cash advances up to $250 |

| Jetzloan | Under 1 day | 12% – 22% | 600 | Fast approval via machine learning |

The table highlights how Jetzloan stacks up against its peers. With a competitive APR range and a minimal credit score requirement, it appeals to borrowers who need speed without sacrificing affordability.

Case Study: Emily’s Emergency Loan

Emily, a 28‑year‑old marketing specialist in Austin, faced an unexpected medical bill of $4,500. She applied for a quick personal loan through Jetzloan and received an approval decision within 30 minutes. Funds were deposited into her account by the next business day, allowing her to settle the invoice without incurring late fees.

Emily noted that the application was straightforward: she uploaded proof of income via a secure portal and answered a few behavioral questions about her spending habits. “I didn’t have to go through a long interview or bring in paperwork,” she said. “The process felt like ordering coffee—quick, simple, and efficient.”

Interest Rates: A Moving Target

While instant loans can carry higher rates than traditional bank loans, the competitive landscape has driven down APRs across the board. According to a 2026 report by Built In, the average interest rate for fintech quick personal loans now sits around 17%, with rates as low as 12% for borrowers with strong credit histories.

Consumers are advised to shop around, compare offers, and read fine print. Even a small difference in APR can translate into hundreds of dollars saved over the life of a loan.

How to Apply: A Step‑by‑Step Guide

- Check Your Credit Score: Know where you stand before applying.

- Determine Loan Amount: Choose an amount that covers your need without overextending.

- Select a Lender: Use comparison tools to find the best rate and terms.

- Gather Documents: Have digital copies of ID, pay stubs, and bank statements ready.

- Complete the Application: Fill out online forms; most platforms auto‑populate data from linked accounts.

- Review Terms: Ensure you understand APR, fees, and repayment schedule.

- Submit: Await approval—some lenders will notify you instantly.

Once approved, the funds typically appear in your bank account within one business day. If you need the money sooner, some lenders offer same‑day funding for an additional fee; however, this should be weighed against potential interest costs.

Common Pitfalls to Avoid

- Ignoring Credit Scores: A low score can lock you into higher rates.

- Overlooking Fees: Hidden service charges can inflate the total cost.

- Missing Repayment Dates: Late payments trigger penalties and damage credit.

By staying informed and diligent, borrowers can navigate the fast‑funding landscape safely and profitably.

The Future of Quick Loans: Trends to Watch

Looking ahead, several developments are poised to reshape instant lending:

- Blockchain Verification: Decentralized ledgers could streamline identity checks.

- Dynamic Interest Rates: AI may adjust rates in real time based on market conditions.

- Expanded Credit Scoring Models: Alternative data—such as rent and utility payments—will broaden access for underserved borrowers.

Fintech companies that embrace these innovations will likely dominate the next wave of rapid funding solutions, offering even faster approvals and more personalized terms.

Industry Voice: An Interview with a FinTech CEO

We spoke with Maya Patel, CEO of Gynger, about the future of instant loans. “Consumers now expect speed comparable to e‑commerce deliveries,” she said. “Our goal is to make loan approval as frictionless as possible while ensuring compliance and affordability.”

Patel highlighted the importance of transparent communication, noting that clear disclosures build trust—an essential factor in a crowded market.

Regulatory Outlook: Upcoming Changes

The CFPB is slated to release new guidelines next year that will standardize interest rate disclosures for instant loans. These rules aim to prevent predatory practices and promote consumer awareness.

- Standardized APR Disclosure: Lenders must present rates in a uniform format.

- Fee Transparency: All fees must be itemized on the application page.

- Consumer Education: Platforms will provide resources explaining repayment obligations.

Fintech lenders who proactively adopt these standards will likely gain a competitive edge, as consumers increasingly value transparency.